If you’ve been paying even a little attention this summer, you’ve probably noticed that Sam Altman is everywhere. He’s running OpenAI… partnering with Apple to put ChatGPT in every iPhone, working closely with the U.S. government on AI safety frameworks, and somehow still finding time to build nuclear reactors with Oklo. And now (because reshaping the future of intelligence, energy, and global policy apparently wasn’t enough) he’s jumping into crypto lending through a startup called Divine Research. (Somewhere in Austin, a Tesla exec probably just got a Slack from Elon that reads: “We need to launch a crypto lender. Today.”)

This time, he’s not chasing AGI or clean energy. He’s trying to reinvent microloans… but instead of using credit scores or actual banks, he’s rolling with eyeball scans and stablecoins. (Yeah, I wish I were making that up.) So here’s what’s happening: Divine is dishing out small loans (under $1,000 in USDC, a dollar-pegged stablecoin) to people mostly outside the U.S. Think countries like Argentina, where inflation is going up faster than Palantir’s stock price.

The big pitch is this: Divine is offering what its founder Diego Estevez calls “microfinance on steroids.” In plain English, that means small-dollar loans (typically under $1,000) are being handed out quickly and without traditional paperwork, thanks to crypto rails and a splash of biometric ID. But here’s the catch: these are unsecured loans. Meaning there's no collateral involved. No car title to repossess, no paycheck to garnish, not even some crypto locked in a smart contract as backup. Just a borrower, a stablecoin, and a scanned eyeball.

Divine uses Sam Altman’s World ID (a biometric identity system that scans users’ irises) to verify each borrower and prevent repeat defaults. The idea is that if someone skips out on a loan, they can’t just open a new account and try again. World ID ensures that one person equals one identity. It’s essentially credit enforcement via eyeball. All that sounds great except for the fact that the default rate on first loans is 40% (in case you were wondering, that’s egregious). That’s nearly half of all new borrowers ghosting their repayments. But wait… it gets better (or worse, depending on whether you're funding this with your rent money).

But have no fear, Estevez claims investors (regular folks chasing unsustainable yields) will still come out ahead. Simply, because they’re charging 20–30% interest to borrowers. Basically the financial strategy is: charge developing-world fruit vendors 30% APR and pray enough of them pay up to cover the ones who disappear. (Side note: If your investment plan involves “hoping people don’t vanish,” it may be time to reassess.)

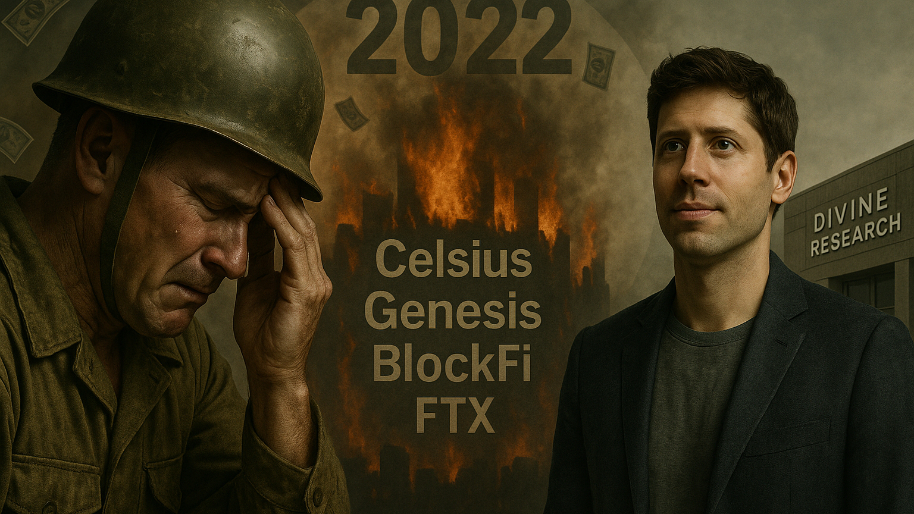

If this is starting to feel familiar, it should. We’ve seen this before. Back in 2022, unsecured crypto lending helped bring the entire market to its knees. Celsius. BlockFi. Genesis. FTX. They all imploded in rapid succession… taking billions in customer funds with them.

FTX alone wiped out $8 billion. Celsius froze withdrawals and turned out to be a Ponzi scheme dressed up as a fintech app. Genesis took a $2 billion legal hit. Even Bitcoin and Ethereum plunged over 75%. It wasn’t just a bad market cycle… it was a systemic collapse (triggered by bad crypto loans).

And here we are, just three years later, running the same playbook… only this time with fancier branding and Sam Altman involved.

Divine is pitching its model as inclusive finance for the unbanked. And on paper, sure… it sounds admirable. Helping people in struggling economies get access to capital? Who’s going to argue with that? But let’s call a spade a spade: what they’re really offering are high-risk, high-interest, unsecured loans to people with little to no financial safety net. That’s not innovation. That’s just a yield-chasing scheme in a new outfit… dressed up with Web3 buzzwords, a little biometric flair, and a pitch deck that hopes you forgot what happened in 2022.

And they’re not the only ones doing it. Take 3Jane, another startup that just raised $5.2 million from Paradigm (yes, the same Paradigm that helped fund FTX). They’re also offering undercollateralized loans in USDC, but with a slight difference: “proof of future income” (which is exactly as squishy as it sounds) and plans to use AI agents to enforce repayment. (If the idea of an OpenAI-trained robo-collector chasing you down for $900 doesn’t terrify you, you haven’t been in enough group chats.)

Then there’s Wildcat, a protocol built for crypto trading firms. Borrowers create their own loan terms, and in the event of a default, lenders just… figure it out amongst themselves. Without third-party enforcement or a safety net. So what does this tell us? The same reckless lending practices that fueled the 2022 crash are quietly returning… just dressed up differently. The risk hasn’t gone away. It’s just hiding behind biometric verification and promises of decentralized utopia (with a wonderboy like Sam Altman behind it).

Meanwhile, real institutions like JPMorgan and Goldman Sachs are only touching crypto lending when it’s backed by actual collateral… as in, real assets they can seize if things go sideways. These firms have seen how the last cycle played out. They remember Mashinsky. They remember SBF. And their legal departments probably still have PTSD.

Now, to be fair… I’m not saying this Divine-style lending is going to crash the entire crypto market all over again. Bitcoin’s hitting new all-time highs, Ethereum’s finally waking up after a multi-year nap, and there’s a tidal wave of institutional capital flowing into BTC. So yes, the foundation is a lot more solid than it was in 2022. No argument there. But let’s not kid ourselves… Divine is still operating in the riskiest part of the ecosystem: unsecured lending with zero meaningful backstop. If this corner of the market cracks? No, it won’t take Bitcoin down with it.

But it will torch some retail investors, tear down confidence in DeFi again, and give regulators all the ammo they need to say, “See? We told you this needed more oversight.” And that’s the last thing this market needs right now in the middle of this rally.

At the time of publishing this article, Stocks.News holds positions in Apple and Tesla as mentioned in the article.

Did you find this insightful?

Bad

Just Okay

Amazing

Disclaimer: Information provided is for informational purposes only, not investment advice. We do not recommend buying or selling stocks. Stock price discussions are based on publicly available data. Readers should conduct their own research or consult a financial advisor before investing. Owners of this site have current positions in stocks mentioned throughout the site, Please Read Full Disclaimer for details Here https://app.stocks.news/page/disclaimer