The Michael Myers of EV Is Skyrocketing +37%... (It Just Won't Die!)

As we approach the beginning of Fall, there’s one company that continues to stay alive regardless of how many setbacks, and blows it takes. And today, the company pacing the plot story of Michael Myers is none other than Polestar.

(Source: Giphy)

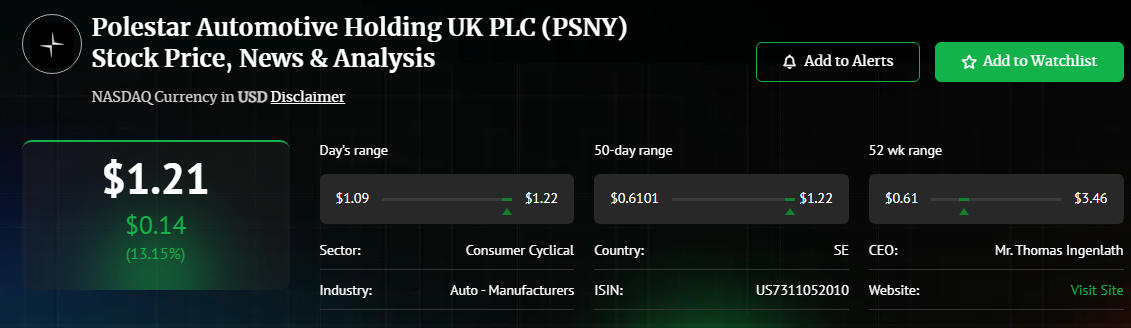

You see, apparently, Polestar just decided to throw its hat back into the ring, making everyone who had already written them off as another EV “wannabe” do a double take. The electric vehicle maker, which has been living in Tesla’s shadow like it’s cockeyed younger sibling, suddenly saw its stock soar by 37.63% over the past five days.

(Source: Google Finance)

The reason? A new CEO appointment of Michael Lohscheller (former CEO of Nikola… yikes) and some optimistic mumbling about the second half of the year. Because you know, imaginary guidance forecasts play a stronger role during earnings than the actual numbers a company reports. Think, complete opposite of Nvidia earnings.

(Source: Seeking Alpha)

Because of this, Polestar’s stock is up - way up, considering where it’s been. But keep in mind, even with a nice +13.15% surge, the stock is still down -46.83% year-to-date and a whopping -87.96% over the last five years. Meaning, you’d have to be an eternal optimist or just really bad at math to see this as a total win. Yet, analysts are out here tossing around a consensus price target of $4.80 per share, which would mean a 306.78% upside - even if it feels like catching a falling knife to some.

(Source: Giphy)

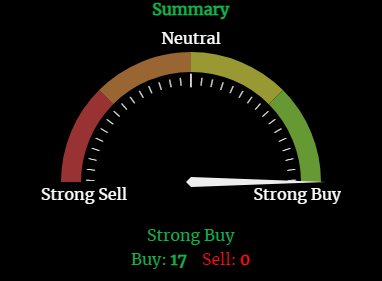

But hey, with all 17 daily indicators and moving averages screaming "Strong Buy," it’s clear Polestar's bandwagon may be starting to grow more and more as the company stays alive. Especially since Polestar's financials have been as ugly as a mud fence recently.

How ugly you ask? Try losing $243 million in Q2, but still quite a bit better than losing $296 million from Q2 2023. Which is somewhat of a good sign I guess, however, revenues did drop by 17%, missing expectations by $67 million. But—and it’s a big but—their gross margin improved to a still-embarrassing -0.7% from a downright atrocious -9%. So if you’re one to look for silver linings, there you go… a Polestar penny in a massive pile of dirt.

(Source: Giphy)

This is not too surprising though as Polestar has historically burned cash faster than my wife does on Prime Day. For instance, Polestar lost over $1.4 billion last year and posted a -21.51% gross profit margin. Translation: They are literally paying people to buy their cars.

However, even with that horrific stat on display, Polestars got a plan - well, sort of. Executives are betting the farm on new models like the Polestar 3 and 4 to finally get some traction.

(Source: Brake and Front End)

Production of the Polestar 3 kicked off in South Carolina this month, which, let’s be honest, is more about dodging tariffs on Chinese-made vehicles than anything else. The Polestar 4? It’s slated for production in South Korea by mid-2025, which feels like a lifetime away in the EV race.

Of course, on a corporate stance, these strategic maneuvers are supposed to keep Polestar in the game - however, from where I’m standing, it feels more like a dropshipper just trying to throw products in the air in hopes of one sticking. But again, for god knows what reason, analysts are still seeing potential in the company's latest pivot.

(Source: Giphy)

I mean sure, Polestar is talking big about hitting double-digit gross margins by November, while being in talks with the EU to ease some of the tariff pain - where Polestar's bright idea back up plan to avoid the 20% EU hike is by making cars in different regions. Read: Polestar 4 made in South Korea. Which is a smart move on paper, but like I’ve said many times in these articles, it’s one thing to talk the talk… it’s a whole ‘nother story to walk the talk. Translation: It’s a bold move for them Cotton, let’s see if it pays off for ‘em.

(Source: Axios)

Plus, even with Geely (Polestar's sugar daddy), who is keeping the company afloat with $950 million in loans and another $300 million in debt financing, all Polestar is to me is a company treading water. That’s it. They have enough cash to keep the lights on and wheels turning, but when it comes to the engine… it’s moving slower than molasses.

So with that said, with Polestar giving itself a target on its back for November (second half earning numbers), we’ll see if their arsenal of new leadership, shiny new models (Polestar 3), and tariff plays will pay off. But in the meantime, all I see is a stock that’s hyped up on imaginary numbers (aka guidance).

(Source: Giphy)

Obviously, only time will tell, but for now enjoy the fact that just like Michael Myers, Polestar can’t seem to die. However, while the stock has hit a peak of +13% on the day, it’s only a matter of time before the dang thing nosedives and adds to the disastrous -91% downfall it’s seen over the last five years. So for you “BTFD” degenerates… please act accordingly.

At the time of this writing, Polestar is up +13.15% on the day, (down -45.25% YTD).

Stocks.News holds a position in Tesla as mentioned in the article.