Peloton’s Down 86% From All Time Highs, Is it Time to Dust Off Your Spandex and Ride Again?

During the height of the pandemic, when home workouts became the norm, Peloton, with its sleek bikes and cult-like following, was riding high—literally. Forget the golf club membership, their bikes were the ultimate status symbol.

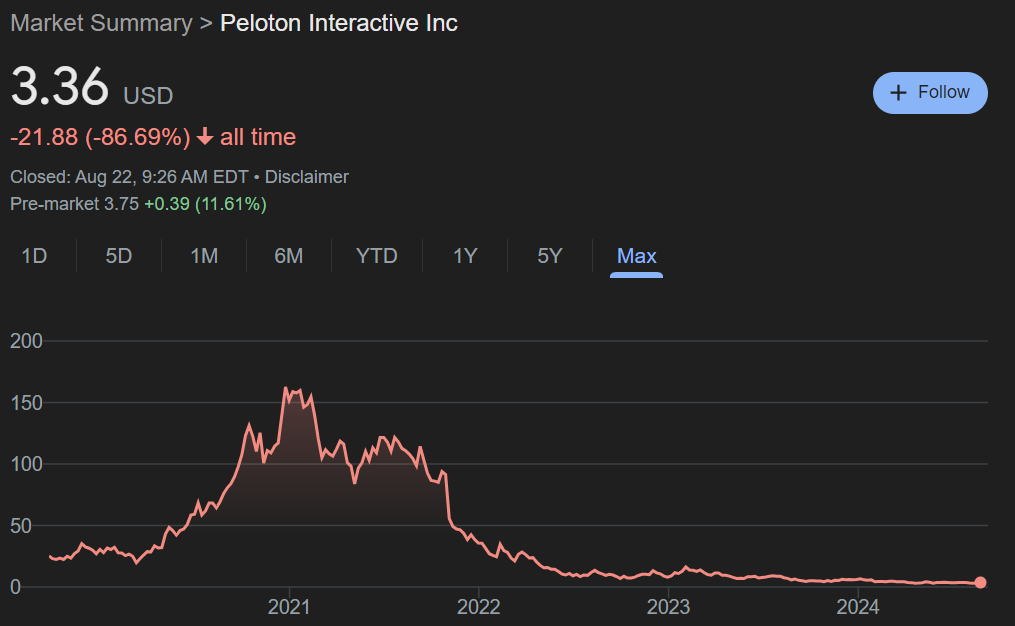

At the peak of the pandemic, its stock soared to a sky-high $171 per share, and the company’s market cap was flirting with $50 billion.

Fast forward to the present, and Peloton’s journey has been less Tour de France and more “Are we there yet?” road trip. Earlier this year, the company’s stock was gasping for air below $3—a record low that had investors wondering if they’d signed up for a spin class or a Nigerian Prince scam. The pandemic boom fizzled out, demand for Peloton’s pricey products tanked, and the company was left scrambling for a lifeline. In 2022, Peloton laid off over 5,000 employees, waved goodbye to four top executives, and even flirted with the idea of a sale to heavyweights like Amazon, Apple, or Nike.

(Source: Business Insider)

Cue the “call an ambulance, but not for me” video because it seems like the underdog is digging itself out of the ditch.

Peloton announced today that it’s managed to scrape together a slight sales increase for the first time in nine quarters. Yep, you read that right—after nearly two years of bleeding cash and losing market share like it was a competition, Peloton has eked out some positive numbers.

Let’s look at the numbers: Peloton reported $644 million in revenue for the quarter ending June 30, which is a smidge under 1% more than a year ago. That might not sound like much, but when you’re coming back from the brink, every penny counts. Wall Street was expecting $630.1 million, so Peloton’s ability to beat that estimate is like pedaling all the way up mount Rushmore with a flat tire.

And the good news doesn’t stop there. Peloton’s adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA, for those who like their acronyms extra crunchy) came in at $70.3 million. Compare that to the $34.7 million loss they posted in the same quarter last year, and you start to see why investors are giving Peloton another look. Heck, shares even jumped about 10% in premarket trading, which is something Peloton investors never thought they’d ever see again.

But before we get too excited, let’s keep it real. Peloton may be showing some signs of recovery, but they’re not out of the woods yet. The hunt for a new CEO is still on after Barry McCarthy decided he’d had enough of Peloton’s drama. And the forecast for the next quarter? It’s more gray skies than clear ones—Peloton’s projecting revenue between $560 million and $580 million, which is a bit of a letdown compared to what analysts were hoping for. Still, the company is focused on profitability over growth, trimming the fat from its bloated marketing budget and cutting expenses left and right.

Peloton’s story is far from over. The brand that once made stationary bikes a must-have status symbol is now fighting to stay relevant in a world that’s moved beyond lockdowns and living room workouts. With its stock down over 86% from its peak, Peloton is doing everything it can to avoid becoming the cautionary tale in a business school lecture on how not to crash and burn.

Stock.News has positions in Amazon and Apple.