FOMO Alert: This Could Be the Most Explosive AI Play of 2024

Well it’s official everyone, Dell Computers has grown up. They are no longer just the company that helped me crank out last-minute term papers in college (God bless them)—they’re now the dark horse sealing its place as a major bada$$ in the world of AI.

(Source: Giphy)

You see, Dell Computers in 2024 have just supercharged the meaning of “Dude you’re getting a Dell?” as the stock has rocketed nearly 50% this year, putting the broader tech sector’s 15% gain to shame.

Which again, is no fluke; especially since it’s the result of a carefully orchestrated pivot from personal computers to the lucrative and rapidly expanding world of AI. Because while Dell has historically been the OG of personal computers, staying in its lane with its reliable laptops that led me here… writing to you beautiful people on this fine Saturday morning -. Dell (unlike Intel) saw the writing on the wall as the PC market matured and growth began to slow.

(Source: MarketBeat)

The solution? Transition from a PC-centric business to an AI leader that is driven by its Infrastructure Solutions Group (ISG). This Dell division is focused on digital transformation for large organizations, leveraging AI, machine learning, and big data analytics to drive growth.

And to put it simply, the results are impressive as revenue in this segment jumped from $4.9 billion in February to $7.7 billion in just six months, a staggering 58% increase that’s harder to ignore than a fat wallet in some Apple Bottom Jeans.

(Source: Reuters)

In short, the ISG’s focus on AI-optimized servers—high-performance machines specifically designed to handle the complex computations required by AI applications—has been key to this growth. These servers are essential for modern data centers, which are increasingly reliant on AI to process massive amounts of data quickly and efficiently. Translation: Dell is selling the shovels to the gold rush. Translation #2: They are cashin’ checks and snappin necks as Dell has smartly positioned itself as a key supplier of these AI-optimized servers.

(Source: Giphy)

So clearly, one could only assume that as more companies across industries—from healthcare to finance to manufacturing—invest in AI, the demand for Dell’s servers is likely to continue growing. This is the main frame of mind that has Wall Street licking its chops.

However, with that said, Dell’s Client Solutions Group (CSG)—the division responsible for those clutch laptops and desktops—still generates the most revenue, but its growth has hit a plateau.

(Source: Market Insider)

For instance, last quarter, CSG brought in $10.5 billion, which is a stark contrast to the explosive growth seen in ISG, which grew 26% from fiscal Q1 2025, with an operating margin of 11%. The difference between the two divisions is telling: while CSG remains a steady performer, ISG is the driving force behind Dell’s future growth.

(Source: Next Platform)

But again, as I mentioned above, the PC market has matured and Dell's CSG’s flat performance reflects broader trends in the PC market, which has become increasingly commoditized and saturated. So while Dell’s laptops and desktops remain popular, especially in the enterprise and education markets, there’s little room for significant growth.

Which is why Dell's ISG focus on AI servers gives the company a lot more Rick Flair over it’s competitors as their AI servers tap into a much more dynamic and rapidly growing market. Literally no shocker there…

(Source: Giphy)

When it comes to the numbers though, it’s even more evident of how much Dell is supercharging it’s “I ain’t f***king leavin’!” mantra as Dell’s latest earnings report didn’t just meet expectations—it bodybagged ‘em.

For example, the company posted $25.1 billion in revenue, smashing forecasts by over $500 million. Adjusted earnings per share (EPS) came in at $1.89, a solid 10% above predictions. The real star of the show? AI-optimized servers, (duh) with sales up 23% from the previous quarter, hitting $3.2 billion.

(Source: Benzinga)

Investors clearly jumped on the train like fleas on a dog, pushing Dell shares up 3.7% in after-hours trading, adding to its +54% gains YTD. Another fuel to the fire came with the remembrance of the $3.8 billion backlog of AI server orders, signifying that Dell’s got more demand than they can handle right now.

Now of course, sure, backlogs can cause headaches—nobody likes waiting around for their shiny new hardware—but Dell is hustling to get ahead of supply chain issues. And with the pipeline for future deals looking even stronger, the company’s AI momentum shows no signs of slowing down.

(Source: Bloomberg)

But again, this backlog is a double-edged sword. On the one hand, it’s a clear sign that demand for Dell’s AI servers is robust and growing (aka a good problem to have). On the other hand, it also highlights the challenges that come with scaling production to meet this demand, especially in a time when global supply chains are still recovering from pandemic-related disruptions. Dell supposedly has plans to conquer this issue by working more closely with suppliers and investing in expansions (no sure details on that yet)...

But despite the supply chain concerns, Wall Street analysts are definitely becoming the Swifties to Dell’s “Taylor Swift” aura. For instance, just recently, Loop Capital’s Ananda Baruah has slapped a buy rating on the stock with a $185 price target - while Goldman Sachs and BofA both upgraded their targets at $155 (yesterday), suggesting Dell’s got another 33% to climb.

(Source: The Fly)

On the other hand, analysts at Wells Fargo actually downgraded its price target by $10 to $140 - which shouldn’t mean much because #1. It’s Wells Fargo and #2. The new price target still hints for +26.42% upside on Dell's stock.

(Source: The Fly)

With that said, for investors, Dell is currently trading at 18 times its earnings, with a streak of EPS beats that’s making analysts nod in approval. Year-over-year, revenue is up 6.32%, while net income, diluted EPS, and net profit margin has grown +64.67%, +67.09%, and +54.84%. Operating income though, seems to be the only lagger as it’s dipped -9.4% YoY. So yeah, there’s that.

However, despite the only blush mark on Dell's white robe, it’s clear Dell’s AI strategy isn’t just working—it’s thriving. As demand for AI servers keeps climbing, Dell is perfectly positioned to capitalize. With a healthy backlog of demand, a robust pipeline, and analysts stepping over each other to issue buy ratings with the average price target indicating a 27.70% upside, Dell is becoming a force to be reckoned with, and it’s definitely not slowing down anytime soon.

(Source: Morningstar)

Meaning, for investors, Dell’s stock is more than just a tech play—it’s a growth opportunity. Up over 54% year-to-date and offering a 1.55% dividend yield, Dell is no doubt a company to watch, and maybe even to own (if it fits with your due diligence - don’t be dumb).

Again, the combination of strong financial performance, and the fact that Dell is adapting better than friggin Intel just shows everyone that the company is serious on making sure they get their hands into the next wave of technological innovation.

(Source: Giphy)

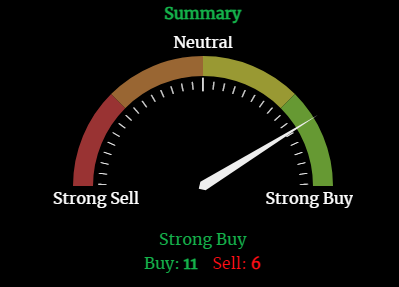

In the end, I’m definitely putting Dell as a contender for becoming one of the most explosive AI plays going forward. Especially considering that 11 out of 17 technical indicators on our Stocks.News daily chart are screaming “Strong Buys”.

Now with that said, do what you want with this information, but please act accordingly. Even though everything from Dell's fundamentals, to its technicals are lining up in perfect harmony, please don’t be dumb. Make sure the stock is right for you before doing anything crazy and YOLOing your whole 401(k) in this stock.

At the end of the day, you know the drill, don’t sleep on Dell. Keep an eye on it, because as we’ve seen, it’s clear they are selling the shovels to one of the most explosive gold rushes in history. And buddy, if that doesn’t get you excited, then I don’t know what will.

Oh, and before I forget, let’s give a massive high-five to all our Stocks.News premium members! Our latest breaking alert, NYSE: TOVX, experienced a squeeze (as we expected) and skyrocketed from $3.56 to $7.15 right after Friday’s opening bell, racking up a 110% gain in under 24 hours. With the market closed for Labor Day, keep an eye out for our next alert on Wednesday, September 4th. Could it be another 100%+ gain in less than a day? There’s only one way to find out.

If you’re not a premium member, hurry and upgrade immediately to get in on the action - especially considering that our last three previous “secret alerts” all exploded to peak moves of +110.10%, +185%, and +300%... in LESS than 48 hours!

In the meantime… stay safe and stay frosty, friends! Until next time…

Stocks.News holds positions in Dell and Intel as mentioned in the article.