Elon’s Ex is Down 80%, But THIS Apple News Just Made it A “BUY”; Wall Street Drops Tech for Hammers

The Dow Jones Industrial Average skyrocketed past 40,000, gaining 258 points (0.6%) as Home Depot (+2.2%) and Caterpillar (+1.6%) led the charge. Apparently, Wall Street loves hammers and bulldozers as much as tech stocks now.

The S&P 500 inched up 0.5%, reclaiming 5,600, while the Nasdaq Composite added 0.6%. The Russell 2000 had a rockin' week, up over 6%, as investors placed bets on the certainty of a soft economic landing.

Banks, however, were down in the dumps: JPMorgan dropped 1.5% despite decent revenue, Citi slipped 1%, and Wells Fargo took a nosedive, plunging 6% because their lending game was off.

And of course, Nvidia bounced back 2%, because apparently it's hard to resist after a sale.

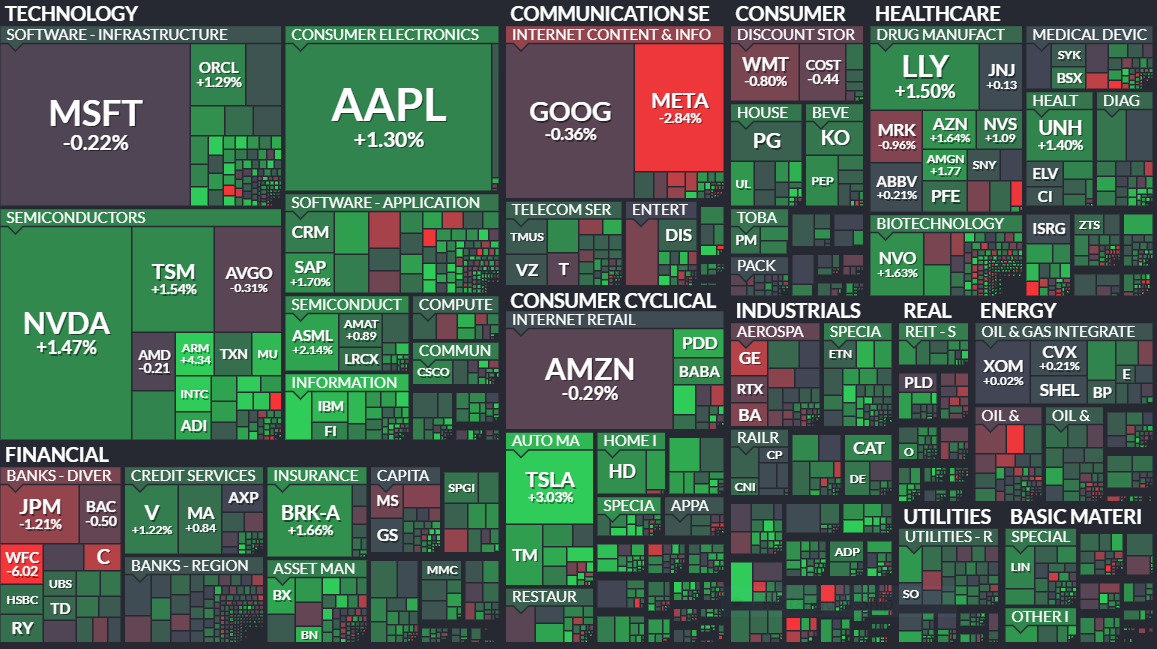

Before we get to the main story, take a look at today’s market heatmap.

Elon’s Ex is Down 80%, But THIS Apple News Just Made it A “BUY”

Around earnings season, news can land like a surprise birthday party—you never know whether it’ll be a wonderful memory that will last a lifetime or an all out disaster.

Well this time it was Apple’s showdown with European Union regulators that sent Elon Musk’s former brainchild, PayPal, soaring.

Apple was forced to comply with the EU’s antitrust rules, agreeing to share its Near Field Communication (NFC) technology—the secret sauce behind tap-to-pay—with other payment providers. Analysts at Mizuho Securities see this as a monumental moment for PayPal. But is this enough to give PayPal investors a glimmer of hope? Let’s look at why PayPal might finally be a good "BUY."

So, what’s the big deal with NFC? Apple’s agreement with the EU means its NFC technology, previously exclusive to Apple Pay, will now be available to other payment services like PayPal’s Venmo.

Think of it as Apple being forced to share its secret stash of candy with the neighborhood kids. This is huge for PayPal, especially since the EU market makes up about 15% to 20% of PayPal’s total revenue. “Quite lovely” isn’t it?

Mizuho analysts are optimistic that this regulatory twist could lead to similar changes in the US. Imagine tapping your phone to pay with Venmo instead of just Apple Pay. With Venmo’s stored balance mix cutting down transaction costs, PayPal’s profit margins could get a nice, fat boost after quite a disappointing year.

When this news hit, PayPal’s stock got a much-needed shot of espresso, rising 1.3% to $59.65. Other payment stocks joined the party too, with Affirm Holdings climbing 3.9% and Block gaining 2.3%. Meanwhile, Apple took a bit of a nosedive, dipping 2.2%. So it’s clear, the market recognized the significance of Apple’s NFC tech opening up.

Now, let’s talk about PayPal’s journey. Once soaring like an eagle, PayPal’s share price has taken a dive, plummeting from its peak like a rock off a Mount Everest. The company, which was once the king of online payments, has faced fierce competition from Apple, Google, and others. The post-pandemic online shopping boom has fizzled out, and PayPal had to pivot to less profitable white-label payment services.

This pivot hammered PayPal’s margins, dropping them from a robust 55.9% in 2020 to a scrawny 45.8% in late 2023. It’s been a bitter pill to swallow—like trying to down a horse-sized vitamin without water—with shares crashing 80% since their peak in 2021.

I’m sure by now, shareholders are probably wishing they had a time machine to go back and give their past selves a good, solid slap for investing in the stock. But that’s all in the past, now, steering the ship through these stormy seas is the new CEO, Alex Chriss.

(Source: CNBC)

Chriss has been rolling out changes aimed at making PayPal leaner and more focused. The company’s Innovation Day didn’t exactly knock Wall Street investors' socks off, but it did outline steps to address core issues: simplifying purchases, boosting profits on white-label offerings, and pushing for faster innovation. The market, however, greeted these plans with a collective yawn, and the stock fell 3.7% that day.

But there might still be a glimmer of hope. PayPal’s new Fastlane service, which automatically fills in personal and credit card information, might just be the secret weapon to boost transaction completion rates. Think of it as PayPal’s version of a fast pass at an amusement park—less waiting, more riding.

JP Morgan’s Tien-Tsin Huang sees potential here, with a $70 price target for PayPal’s stock. Monness Crespi Hardt analyst Gus Galá, despite calling the company’s guidance disappointing, set an $80 target, banking on better-than-expected results from PayPal’s innovations.

So, what does all this mean? Apple’s antitrust settlement with the EU is a beacon of hope for PayPal. It opens new avenues in a key market and potentially in the US, which could significantly bolster PayPal’s margins. But let’s cut to the chase: PayPal’s stock is so cheap right now, it’s practically in the bargain bin. With shares having plummeted 80% since their peak in 2021, it’s hard to see how it could drop much further. It’s like buying a used car that’s already depreciated—there’s not much left to lose.

Stock.News has positions in Apple and Google.